President Donald Trump signed an government order on April 30, 2026 directing the Treasury Division to run TrumpIRA.gov. This new on-line platform goals to broaden entry to retirement financial savings for the tens of hundreds of thousands of American staff whose employers don’t supply a 401(ok) or comparable plan.

The initiative builds on earlier efforts, together with Saver’s Match (because the 2022 Safe 2.0 Act), and focuses on sensible, long-term wealth constructing—following timeless rules from buyers like Jack Bogle (low-cost indexing), Warren Buffett (affected person, disciplined saving), and Benjamin Graham (specializing in worth and avoiding pointless danger). Whereas not a completely new kind of account within the conventional sense, it creates a neater path to current IRAs and makes use of authorities matching for eligible low-income savers.

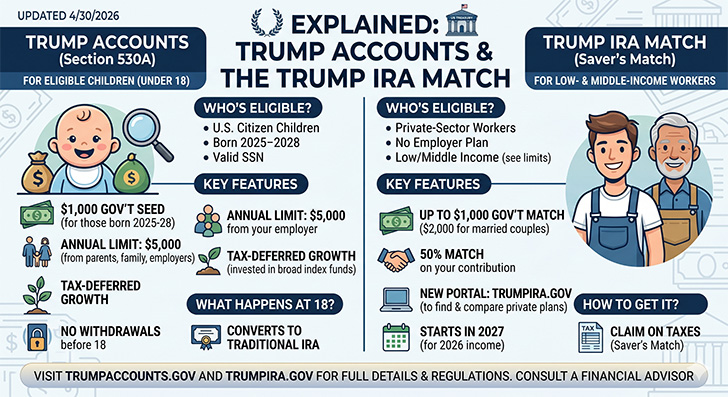

Who’s eligible for TrumpIRA.gov and associated advantages?

- Main customers: Employees with out employer-sponsored pension plans (estimated at about 40% of full-time staff and 80% of part-time staff).

- Saver’s Match Eligibility (from 2027): Decrease-income people can stand up to $1,000 a yr in authorities advantages. For 2027, this usually applies to people incomes lower than $35,500 or joint filers underneath $71,000 (actual limits could alter based mostly on inflation or tips). The match is the same as as much as 50% of your contributions, that are deposited straight into your retirement account.

- Broader entry: Any employee can use this website to match and enroll in personal IRAs or comparable plans. Future extensions might embrace auto-enrollment options or incentives for personal donors to donate.

The platform will act as a market, permitting customers to filter plans by charges, minimums, funding choices and extra – encouraging knowledgeable, low-cost decisions over high-fee merchandise.

How TrumpIRAs are completely different from current retirement choices

TrumpIRA.gov would not invent a completely new account construction, nevertheless it simplifies entry conventional or Roth IRAs (and probably different plans) for underserved staff. This is a comparability:

- vs. Conventional Employer 401(ok): No employer match is required (though some plans could supply it). Simpler setup with out office involvement. Contribution limits observe normal IRA guidelines (eg $7,000 for under-50s in recent times plus catch-up for older savers – test present IRS limits).

- vs. Customary IRA: The important thing distinction is less complicated enrollment and consciousness by TrumpIRA.gov, plus Saver’s Match help for certified low-income earners. No earned revenue requirement adjustments, however the website lowers limitations for gig staff, part-timers and small enterprise staff.

- vs. Subordinate “Trump Accounts” (standalone program): Be aware that “Trump Accounts” (underneath the One Large Stunning Act of 2025) are separate custodial IRAs for minors underneath 18, with a federal seed of $1,000 for births 2025-2028, annual contributions of as much as $5,000, and strict funding guidelines (e.g., low-cost US index funds). These began contributions on July 4, 2026 and roll over to a regular IRA at age 18. The April 30 discover is geared toward grownup staff.

Tax therapy mirrors Customary IRA: Conventional for advance deductions (if eligible) and tax-deferred progress; Roth for certified tax-free withdrawals. Picks earlier than 59½ usually face penalties, which inspires long-term holding.

Key options and sensible particulars

- Begin the timeline: The web site is underneath growth, with full Saver’s Match integration deliberate for 2027.

- Funding strategy: Customers select private-sector plans, ideally with an emphasis on low-cost index funds or broad-market ETFs—in line with Bogle’s philosophy of “do not search for a needle in a haystack, simply purchase a haystack” and Malkiel’s efficient insights into the random stroll market. Keep away from excessive charges or speculative choices to maximise compounding.

- Authorities roles: Treasury controls the platform and the match. Personal donors could contribute sooner or later as directed.

- Tips on how to get began (anticipated): Go to TrumpIRA.gov reside as soon as, evaluate plans, open an account, contribute (by way of payroll if potential or straight) and get a match, if eligible, by way of tax return or direct deposit.

Why It Issues: A Lengthy-Time period Investing Perspective

Retirement safety stays a problem for a lot of. With roughly half of personal sector staff not having quick access to plans, this addresses an actual hole with out overcomplicating the system.

From a standard sense perspective:

- Begin early and constantly: Even modest contributions (enhanced by wrestling) add as much as compound progress over many years.

- Preserve prices low: The place potential, want plans with an expense ratio under 0.1%.

- Diversify extensively: The US whole market or S&P 500 index funds have traditionally produced sturdy long-term returns with manageable volatility.

- A pair with religion and self-discipline: As stewards of sources, constant saving displays knowledge (Proverbs 21:20) whereas avoiding debt traps or get-rich-quick schemes.

It isn’t revolutionary like the brand new Roth choice, nevertheless it’s pragmatic—it makes use of current infrastructure, public-private partnerships, and incentives to assist extra households construct wealth. Enhances the subordinate Trump payments for multigenerational planning.

Motion steps for readers

- Examine your employer’s plan standing.

- Watch TrumpIRA.gov for launch particulars and directions.

- In the event you qualify for the Saver’s Match, plan your contributions to maximise the potential of $1,000.

- Seek the advice of a tax advisor or fiduciary to tailor your general portfolio.

- Think about combining with different automobiles (529 for teenagers, HSA for well being) for a holistic technique.

As Burton Malkiel and others remind us, funding success comes from time available in the market, not timing the market. Instruments like TrumpIRA.gov make it simpler for extra People to take part. Keep knowledgeable, make investments steadily and give attention to the lengthy sport – your future self (and household) will thanks.

This text is for informational functions. Tax legal guidelines and program particulars are topic to alter; test with IRS.gov or an expert.